The clinical trials of semaglutide and tirzepatide produced 15-21% weight loss. STEP 1 hit 14.9% with semaglutide; SURMOUNT-1 hit 20.9% with tirzepatide. SELECT, the cardiovascular outcomes trial of semaglutide, produced a 20% reduction in major adverse cardiovascular events. These are remarkable numbers — among the most impressive results in obesity drug research — and they have driven the cultural and commercial story of GLP-1 medications since the first headlines broke.

Real-world results look different. The largest claims-based analysis to date, a 2025 Cleveland Clinic study of 7,881 adults on semaglutide or tirzepatide for obesity (Gasoyan et al., Obesity), found mean 1-year weight loss of 8.7% — roughly half the trial figure. But the average obscures what is actually happening underneath it. Most patients never reach the maintenance dose used in the trials.

Source: Gasoyan et al., Obesity, 2025 (DOI: 10.1002/oby.24331). 80.8% of all patients were on low maintenance doses — never reaching the dose used in the pivotal trials. Only the 19% who reached high maintenance dose achieved trial-equivalent weight loss. See the full real-world outcomes data and persistence data.

The 19% of all initiators who reached high maintenance dose got trial-equivalent results: 13.7% on semaglutide, 18.0% on tirzepatide. The other 81% — patients who stayed on low doses, discontinued early, or discontinued late — got progressively less. A separate 2024 Danish national registry analysis confirms the same pattern outside the United States: just 12% of Wegovy initiators reached the trial maintenance dose by their fifth prescription.

The drug works. It works at trial-level efficacy in the patients who tolerate the side effects, push through dose titration, and stay on. The headline weight loss numbers are real for that minority. For everyone else — the majority — the drug delivers a fraction of the result, or none of it at all.

This is the Reality Gap: the structural difference between GLP-1 efficacy under clinical-trial conditions and GLP-1 effectiveness under real-world conditions. It is the most important fact about obesity drugs in 2026, and it explains nearly every news story in the space — from employer coverage decisions, to rising pharmacy budgets, to the mainstream press writing about food enjoyment loss and identity changes alongside the miracle-cure stories that still dominate.

The Three Layers

The Reality Gap has three layers — infrastructure, cost, and behavior. They are distinct but connected.

The Infrastructure Gap

The clinical trials of GLP-1s for obesity were not just drug trials. They were trials of a drug delivered inside a clinical and operational system — paid study coordinators, scheduled monitoring visits, structured dose titration, side-effect management protocols, and dedicated retention contact. The system existed because the sponsors needed the trial to succeed, and they understood that in obesity pharmacotherapy, the drug alone is not the intervention. The intervention is the drug plus the system that gets the patient on it, up to the right dose, and through the side effects.

This system is expensive. Novo Nordisk and Eli Lilly do not disclose per-patient trial costs, but bottoms-up estimates derived from per-patient cost benchmarks for endocrine and metabolic Phase 3 trials (Moore et al., BMJ Open 2020; Sertkaya & Berger, HHS/ASPE 2024) and the published protocols of STEP 1 and SURMOUNT-1 put the non-drug cost at roughly $31,000 to $36,000 per patient — somewhere on the order of four to five dollars of clinical and operational support for every dollar of drug.

Most real-world patients receive a prescription, a pharmacy fill, and perhaps an annual physical. Some employers pair GLP-1 coverage with behavioral programs, but they remain a minority — and WTW data shows that requiring them can forfeit manufacturer rebates. The clinical and operational apparatus that made trial titration and trial retention possible is not part of the standard pharmacy benefit. The drug crosses from trial to real world, but the system around it does not.

The Cleveland Clinic data shows what this difference produces in outcomes. The 19% of patients who reach high maintenance doses achieve trial-equivalent weight loss; the 81% who do not, do not. We do not have direct evidence on what enabled the high-dose minority to get there — the data does not tell us whether they had unusual side-effect tolerance, more attentive prescribers, better access, or some combination. What the trial data does tell us is that when the clinical and operational system around the drug is intensive enough, trial-level results are achievable. Outside that system, achieving them depends on luck, individual circumstance, or paid alternatives that most patients do not have.

The Cost Gap

Trial economics ignored cost. Real-world economics are dominated by it.

In the trial, drug and program were free. Outside the trial, GLP-1s have become the single largest pharmacy spend line item for many self-insured employers.

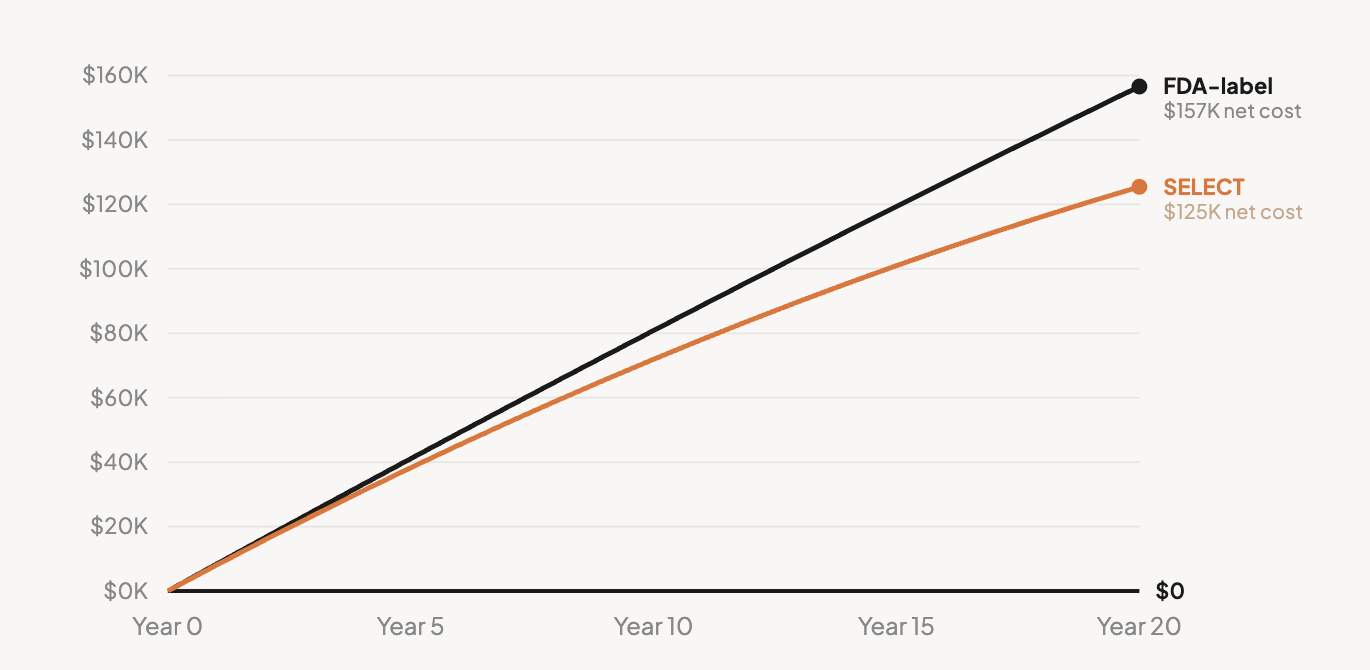

Source: WTW Rx Collaborative, "GLP-1 Drugs in 2025." A 19-fold increase in six years. See the full cost reference data.

GLP-1s now account for roughly 21% of total pharmacy spend across the WTW Rx Collaborative as of Q1 2025. Patients face the cost question on the other side of the same transaction. In the same Cleveland Clinic chart review (Gasoyan et al., 2025), 48% of obesity-indication patients who discontinued cited cost or insurance as the primary reason — the most common reason given. Many lost coverage when employers dropped or restricted benefits; many faced copays or coinsurance that became unsustainable.

Then there is the structural distortion of the current pharmacy benefit model. Employers paying through a pharmacy benefit manager often pay more for Wegovy than the same employee would pay buying it in cash from NovoCare directly: $617-$796 per month employer net (after rebates) versus $349 per month direct-to-consumer. The employer is paying a markup that the cash market does not see. Full cost data here.

The Behavior Gap

Obesity is not a condition with a defined treatment endpoint. There is no twelve-week course, no surgical resolution, no single intervention that completes the work. Patients are asked to take a medication indefinitely, and the medication produces results only as long as it is taken. This makes obesity pharmacotherapy uniquely dependent on long-term patient behavior — and uniquely vulnerable to whatever causes that behavior to change.

What patient behavior actually looks like is poorly aligned with the indefinite-use model. Of the 2021 cohort of obesity GLP-1 initiators tracked by Prime Therapeutics, 8.1% remained on therapy at three years. Newer cohorts show genuinely improving 12-month persistence, in the range of 58-64%, though three-year data on those cohorts does not yet exist. Cycling — start, stop, restart — is common: roughly a third of discontinuers restart within a year. Whether second courses produce equivalent weight loss to first remains unpublished.

There is also a dimension of patient experience that is well-documented in patient communities but has not yet been studied at population scale in the peer-reviewed literature. Patients who continue on GLP-1s describe the experience in mixed terms: loss of food enjoyment, social disruption, what mainstream coverage in early 2026 began calling "Ozempic personality" — a flattening of food enjoyment, social ritual, and sometimes broader affect (Boston Globe, Washington Post, April 2026).

The chart-review categories used in the major discontinuation studies have no buckets for identity, food enjoyment, or quality of life. Patients are, in many cases, taking a drug they describe as remarkable while quietly mourning what it has changed about their daily experience. For some, those tradeoffs eventually contribute to stopping. When patients do stop, weight regain is well documented — real-world studies show 67% to 100% of the lost weight returns within 12 to 18 months across every published study.

Trials measured one to three years. Patients live for decades.

The ROI Question

The three layers above explain why real-world weight loss is a fraction of trial weight loss, why the drug is too expensive to scale, and why patients eventually stop. The deeper question — and the one with the most uncomfortable answer — is whether broad GLP-1 coverage produces positive return on investment for employers at current prices, observed real-world utilization, and ordinary employer time horizons.

Cost-effectiveness analysis asks whether a treatment delivers enough health benefit to justify its cost, typically measured in dollars per quality-adjusted life year (QALY) gained. The standard threshold for "cost-effective" in the United States is $100,000-$150,000 per QALY. The Incremental Cost-Effectiveness Ratio (ICER) is the calculated dollar cost per QALY gained for a given treatment versus an alternative. A treatment with an ICER of $50,000/QALY is considered very cost-effective. A treatment with an ICER of $300,000/QALY is generally not.

The most rigorous independent cost-effectiveness analysis of GLP-1s for obesity (Hwang et al., JAMA Health Forum 2025) found tirzepatide produces an ICER of $197,023 per QALY and semaglutide produces $467,676 per QALY — both well above the $100,000 threshold. To reach the threshold, tirzepatide would need to drop another ~30% to roughly $361 per month; semaglutide would need to drop another ~82% to roughly $127 per month. Even Novo Nordisk's announced January 2027 price reduction to a $675 monthly WAC, after rebates, lands at an estimated employer net of around $4,781 per year — still well above the threshold semaglutide would need to reach.

Cost-Effectiveness Is Not Employer ROI

Cost-effectiveness and employer ROI are different questions, and conflating them is the most common move in vendor analyses. Cost-effectiveness asks whether a treatment delivers good societal value over a lifetime. Employer ROI asks whether the plan recoups its drug spend in medical offsets within a 1-5 year budget window. A therapy can be cost-effective over a lifetime — ICER's December 2025 analysis arrives at $61,400/QALY for semaglutide on this longer horizon — and still fail the ROI test for an employer with a four-year average employee tenure. Most cardiovascular and metabolic benefits from weight loss take 5-15 years to materialize at population scale. The employer who covers the drug now is rarely the one who captures the savings.

The independent evidence on actual employer ROI consistently says no offset has been demonstrated.

Full citations and context on the ROI reference page.

If positive ROI has not been demonstrated under observed real-world utilization, the standard commercial case for broad employer coverage is hard to defend regardless of how well the drug works clinically. The published evidence currently answers this question negatively, and no manufacturer, PBM, or vendor has produced a counter-analysis that addresses total cost of care rather than medical costs alone.

The Framework in Action

Two recent developments illustrate how the framework explains what is happening in the GLP-1 market.

When Massachusetts' Group Insurance Commission — the public agency that runs the health benefit plans for state employees, retirees, and their dependents, covering more than 460,000 lives — dropped GLP-1 weight loss coverage for January 2026, citing close to $1 billion in projected 2026 spending, the decision looked like a payer giving up on a promising drug. Through the Reality Gap lens, it is something different: a payer recognizing that the cost layer alone makes the math impossible regardless of clinical efficacy. The decision was not skepticism about whether GLP-1s work — they do. It was recognition that the system around the drug does not produce returns. BCBS Massachusetts, Idaho state employees, North Carolina state plans, and others have already made similar decisions. More will follow.

The PMPM trajectory tells the same story at the macro level. GLP-1 pharmacy spend went from $1.43 PMPM in 2019 to $27.23 PMPM in Q1 2025 (WTW Rx Collaborative). This is not a story about misuse, fraud, or inappropriate prescribing. It is what happens when a drug priced for trial economics meets a real-world demand curve, with no infrastructure to identify responders, no behavioral support to maintain outcomes, and no off-ramp for the inevitable discontinuations. Much of that 19-fold increase is paying for access under a benefit design that has not yet demonstrated employer-level ROI. This is the Reality Gap expressed as a budget line. See the full pharmacy spend data.

The Drugs Are Remarkable. The System Around Them Is Incomplete.

Most analysis of GLP-1 medications has been either too positive or too negative. The Reality Gap framework is neither. The drugs are remarkable. The system around them is incomplete. Both things are true, and the gap between them is where the next decade of obesity policy, employer benefits, and metabolic care will be decided.

I'll keep applying this framework as the data evolves.

This analysis draws on Key to Health's open GLP-1 reference series — including the costs page, persistence page, weight regain page, ROI page, and real-world outcomes page. All numbers cited above are sourced and footnoted on the relevant reference pages.

Key to Health is an evidence-based behavioral weight management program. Published RCT data in 155 adults; 2-year real-world outcomes from 11,365 adults under peer review. Learn more about our employer program.