GLP-1 medications are the most clinically impressive cardiometabolic drugs in a generation. Semaglutide produced a 20% reduction in major adverse cardiovascular events in the SELECT trial (Lincoff et al., NEJM 2023). Tirzepatide produced up to 22.5% weight loss at the 15 mg dose in SURMOUNT-1. These are large, well-conducted, replicated results. The clinical case for GLP-1 therapy in patients with the right risk profile is strong and getting stronger.

The question facing health plan decision-makers is different. Not "does the drug work," but "does broad GLP-1 coverage produce a positive financial return on pharmacy and medical spend?" This question matters for self-insured employers designing benefits, for health plans setting formulary policy, and for any payer evaluating whether GLP-1 coverage pays for itself in reduced medical claims. This article is a bottoms-up answer, modeling four scenarios across two populations and multiple time horizons. The analysis extends the structural framework described in The Reality Gap.

GLP-1s may be among the most valuable drugs ever developed and still fail the payer-budget ROI test for broad coverage at current prices.

A scope note: this analysis models obesity-only populations without type 2 diabetes. The ROI profile for T2D is different and not addressed here.

In the broad FDA-label obesity population, modeled medical savings from MACE and T2D prevention total about $83 per patient-year under real-world conditions, or roughly $7/month. The drug costs $8,400/year. Even in an ideal scenario where every patient stays on the recommended dose indefinitely, the breakeven drug price is only $48/month for the broad population and $177/month for the highest-risk SELECT-eligible subgroup (patients with BMI ≥27, established cardiovascular disease, no diabetes, age ≥45). At current pricing, broad GLP-1 coverage is a valuable employee benefit, but not a self-funding medical-cost strategy. The analysis below shows why.

1. SELECT-eligible patients vs. FDA-label patients: why they are financially different

2. Real-world vs. ideal persistence and recommended dosing

3. What MACE and T2D offsets actually amount to, even under ideal conditions

4. What unmodeled benefits would need to be worth for ROI to work

5. What the breakeven drug price is under base-case and favorable assumptions

Two populations, two different questions

The coverage population. For chronic weight management, the FDA label for Wegovy and Zepbound covers adults with BMI ≥30, or BMI ≥27 with at least one weight-related comorbidity. An estimated 93 million US adults meet similar eligibility criteria, roughly 38% of all US adults, with comparable or higher prevalence in working-age populations where obesity peaks in middle age (Wong et al., Cardiovasc Drugs Ther 2023).

The cardiovascular-benefit population. SELECT enrolled patients with BMI ≥27, established cardiovascular disease, no type 2 diabetes, and age ≥45. This population represents roughly 5.6% of all US adults, or approximately 7.9 million people. Because established CVD is concentrated in older adults, the share of a commercially insured working-age population that fits is substantially lower (Erhabor et al., JAMA Network Open 2024). Conservative estimates put SELECT-eligible patients at 1-3% of covered lives.

SELECT-eligible patients compose roughly 8-9% of the broader medication-eligible population (7.9 million of 93 million). The large majority of the population being proposed for coverage are primary-prevention patients in whom MACE reduction has not been demonstrated in a dedicated trial. This does not mean the drug doesn't benefit them clinically. But the strongest case for coverage applies to a small minority of the coverage population.

Four scenarios: persistence × dose

Two variables determine how much of the trial benefit a real-world patient receives. Persistence is whether a patient stays on therapy long enough. Recommended dosing is whether they reach the maintenance dose used in clinical trials (2.4 mg for semaglutide, 15 mg for tirzepatide). Both are substantially lower in practice than in trials.

Real-world persistence has improved in recent cohorts but remains well below trial levels. Recent Prime Therapeutics data show approximately 63% one-year persistence among 2024 Wegovy/Zepbound initiators, a genuine improvement over older cohorts affected by supply shortages, while longer-term data from earlier cohorts show only 15% at two years and 8.1% at three years (full persistence data; Gleason et al., JMCP 2026). Whether newer cohorts sustain gains beyond 12 months is unknown.

For semaglutide specifically, rates of reaching the recommended dose are well below trial levels. In a Danish national cohort of 110,748 Wegovy initiators, only 13% reached the recommended 2.4 mg dose by their fifth prescription (Ladebo et al., Diabetes Care 2024). US data is similar: in a Vanderbilt academic obesity clinic cohort, only 23% of semaglutide users ever escalated to 2.4 mg (Samuels et al., Diabetes Obes Metab 2025).

dose

dose

Scenario D represents ideal performance: every patient reaches the recommended dose and stays on therapy indefinitely. If the math does not work when every patient stays on therapy forever at the trial dose, the problem is not adherence, coaching, prior authorization, or engagement. It is structural.

The model

We compute net cost per starter (drug spend minus medical-cost offsets) across four time horizons. This is not a societal cost-effectiveness model. It is a payer-budget model: drug spend versus medical-cost offsets captured by the plan. The benefits draw on the two GLP-1 effects with the strongest outcomes evidence and clearest claims translation: cardiovascular event prevention (20% relative risk reduction per SELECT) and incident type 2 diabetes prevention (73% reduction, also per SELECT). Additional clinical benefits are addressed separately in the breakeven-gap calculation.

- Drug cost

- $8,400/year ($700/month modeled employer net after rebates; actual net varies by PBM and plan design)

- MACE event cost

- $60,000 per event, blended across nonfatal MI (~$50K acute + 1-year), nonfatal stroke (~$85K), and CV death (~$40K)

- T2D incremental cost

- $7,000 per patient per year in the early years after diagnosis, based on commercial populations

- MACE relative risk reduction

- 20%, from SELECT (semaglutide 2.4 mg vs. placebo, mean 3.3-year follow-up)

- T2D relative risk reduction

- 73%, from SELECT (new-onset diabetes, semaglutide vs. placebo)

- Real-world persistence

- Recent Prime data show ~62.6% one-year persistence among 2024 initiators; older cohorts show ~15% at two years and 8.1% at three years. The model uses a blended/extrapolated curve based on these observations

- Real-world dose effect

- We estimate that real-world patients receive about 75% of the clinical benefit observed in trials, because most patients remain on doses below the recommended maintenance dose. This is a simplifying assumption, not a directly measured clinical parameter

- T2D savings accumulation

- In Scenario D (on drug indefinitely), each prevented T2D case averts ~$7K/year for all remaining years, so savings grow over time. If the effect is primarily delay rather than permanent prevention, long-run savings would be lower. Under real-world persistence, savings are proportional to time on drug only

Sources: reference pages on cost, persistence, and real-world outcomes. MACE event costs from Kazi 2019, Johnson 2016, Pham 2023. T2D cost from Nichols et al. 2020. All inputs use mid-range or drug-favorable assumptions: SELECT's relative risk reductions are extrapolated beyond the trial's 3.3-year follow-up, applied at full magnitude for up to 20 years, and extended to the FDA-label population where no dedicated primary-prevention MACE trial exists. Drug price is held constant at $700/month. Novo Nordisk has announced a WAC cut to $675/month effective January 2027, but post-cut rebate terms are unknown and Eli Lilly has not announced comparable cuts. Price reductions are addressed in the breakeven section. All figures are undiscounted.

Included: drug spend, MACE event prevention (per SELECT), and incident T2D prevention (per SELECT).

Not included in the base case: QALY/quality-of-life value, productivity, recruitment/retention, OSA, knee OA, HFpEF, MASH, CKD, adverse events, program administration costs, or patient out-of-pocket value.

That choice is intentional: MACE and T2D are the two benefit pathways with the strongest direct outcomes evidence for hard medical-cost offsets and the clearest translation to payer medical-claims budgets. Other benefits are addressed separately in the breakeven-gap calculation.

SELECT-eligible: the favorable case

The SELECT-eligible population has the highest baseline event rates and therefore the strongest financial case for GLP-1 coverage. Baseline MACE runs 24 per 1,000 person-years (SELECT placebo arm). T2D incidence runs 3.6% per year. This population represents roughly 1-3% of commercially insured covered lives.

The table below shows Scenario D: every patient at the recommended maintenance dose, staying on therapy indefinitely. This is the best case for financial return from MACE and T2D prevention, and is intentionally drug-favorable. It assumes sustained treatment effect, SELECT-level relative risk reductions extrapolated over 20 years, and T2D prevention treated as durable avoided cost while on therapy.

| Horizon | Drug spend | MACE savings | T2D savings | Net cost |

|---|---|---|---|---|

| Year 1 | $8,400 | $288 | $92 | $8,020 |

| Year 5 | $42,000 | $1,440 | $2,300 | $38,260 |

| Year 10 | $84,000 | $2,880 | $9,200 | $71,920 |

| Year 20 | $168,000 | $5,760 | $36,800 | $125,440 |

Credits MACE and T2D prevention only. Potential savings from OSA, knee OA, HFpEF, MASH, CKD, productivity, and recruitment/retention are not included. See what would have to be true for what those benefits would need to total.

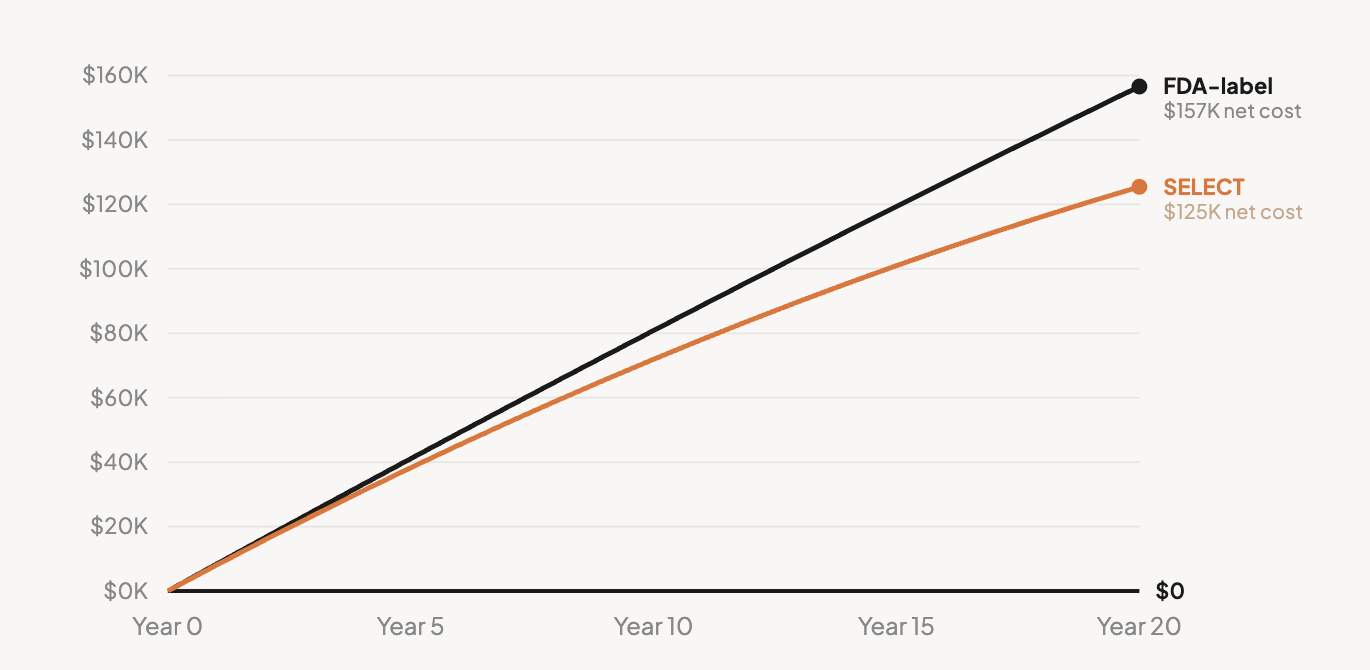

Over 20 years at ideal persistence and dose, MACE prevention saves $5,760 per starter. T2D prevention saves $36,800 (the larger benefit, because each prevented case accumulates as avoided cost year after year). Total modeled medical offset: $42,560. Total drug cost: $168,000. Net: $125,440 in cost per starter, before crediting any unmodeled benefits.

The underlying arithmetic explains why. SELECT reported a number needed to treat of approximately 67 over 3.3 years to prevent one MACE event. At $8,400/year per patient, the drug cost to prevent one event is roughly $1.85 million. The event itself costs ~$60,000. The ratio, roughly 31 to 1, is the structural constraint.

| Scenario | Year 1 | Year 5 | Year 10 | Year 20 |

|---|---|---|---|---|

| AReal-world dose & persistence | $6,558 | $11,908 | $13,163 | $15,175 |

| BIdeal dose, real-world persistence | $6,461 | $11,733 | $12,970 | $14,952 |

| CReal-world dose, ideal persistence | $8,115 | $39,195 | $74,942 | $136,086 |

| DIdeal dose & persistence | $8,020 | $38,260 | $71,920 | $125,440 |

Net cost per GLP-1 starter (drug spend minus MACE and T2D offsets), undiscounted, before crediting unmodeled benefits.

Two patterns are worth noting. First, A and B are nearly identical. Improving dose without improving persistence barely moves the needle, because cumulative drug-years are bounded by dropout (approximately 1.9 patient-years of drug exposure per starter over 20 years). Second, Scenario D is dramatically more expensive than the status quo. In Scenario A, discontinuation caps the plan's financial exposure at roughly $15,000 per starter over 20 years. In D, drug spend grows to $168,000, and the additional $42,560 in medical offset does not come close to closing the gap.

FDA-label population: the broader coverage question

The FDA-label population is the coverage question most benefit committees are evaluating. It describes roughly 38% of US adults. Annual MACE event rates in commercially insured working-age adults without prior CVD are substantially lower: roughly 3-10 per 1,000 person-years (we use 5 as the base case, noting that clean commercial-only data for this stratum is limited). T2D incidence runs roughly 1% per year.

| Horizon | Drug spend | MACE savings | T2D savings | Net cost |

|---|---|---|---|---|

| Year 1 | $8,400 | $60 | $26 | $8,314 |

| Year 5 | $42,000 | $300 | $639 | $41,061 |

| Year 10 | $84,000 | $600 | $2,555 | $80,845 |

| Year 20 | $168,000 | $1,200 | $10,220 | $156,580 |

MACE + T2D offsets only. MACE rate: 5/1,000 PY (primary prevention, limited evidence, a key sensitivity variable). T2D rate: 1.0%/yr. Applying SELECT's 20% MACE relative risk reduction to primary-prevention patients is a favorable extrapolation; no dedicated primary-prevention MACE outcomes trial has established this effect. See what would have to be true for unmodeled benefits.

The magnitudes are worse. At 20 years in Scenario D: $168,000 in drug cost, $11,420 in total modeled medical offset, $156,580 in net cost per starter. MACE offsets are negligible ($1,200 per starter over 20 years) because the underlying event rate in primary-prevention working-age adults is low.

Reality check

Does this model align with real-world data? Yes. Prime Therapeutics' independent claims analysis across 16.5 million commercially insured members found Year-1 incremental cost per user of $6,994 and Year-2 incremental cost of $4,206, with two-year cumulative net investment of $11,200 (AMCP 2024-2025 data). Our Scenario A (real-world) output for the FDA-label population produces a comparable Year-1 net cost. The model is not producing an abstract theoretical warning. It is reproducing what payers are already seeing in claims data.

Cost-effectiveness analysis measures value differently than payer ROI. It uses quality-adjusted life years (QALYs), where one QALY equals one year of life in perfect health, and a treatment is considered "cost-effective" if it costs less than $100,000-$150,000 per QALY gained. At current US net prices, independent analyses have generally not found GLP-1s for obesity cost-effective even by that standard. Hwang and colleagues found tirzepatide at $197,023/QALY and semaglutide at $467,676/QALY in the broader obesity population, with 0% probability of cost-effectiveness (Hwang et al., JAMA Health Forum 2025). In SELECT-eligible patients specifically, a 2026 analysis found $148,100/QALY (Hennessy et al., JAMA Cardiology 2026). A Novo Nordisk-funded analysis reaches $32,219/QALY, but only under a 48% rebate assumption; at list price the same model produces $136,271/QALY (Journal of Medical Economics 2025). Payer medical-claims budgets do not capture QALY value. Our payer-budget analysis reaches the same structural conclusion from a more direct angle.

Neither population reaches breakeven at any horizon. Drug spend grows linearly; medical offsets grow but never inflect toward closing the gap.

What would have to be true for GLP-1 ROI to work

For broad GLP-1 coverage to produce positive financial return, several conditions would need to hold simultaneously. Each is necessary. None alone is sufficient.

1. Coverage would need to be tightly gated to the highest-risk subpopulation

The SELECT-eligible population is the only one with dedicated MACE-reduction trial evidence, and it represents roughly 8-9% of the broader coverage-eligible population (plausibly lower in working-age commercial plans). Broad coverage of the full FDA-label population at any plausible price produces deeply negative financial returns because primary-prevention event rates are too low to generate offsets approaching the drug cost.

Within the SELECT-eligible population, one subgroup has the highest per-patient offset potential: patients who already have heart failure. The prespecified SELECT analysis showed an HR of 0.79 for an HF composite endpoint in this group, and HF hospitalizations are expensive at ~$13,000-$15,000 per event for commercial payers (Deanfield et al., Lancet 2024). But even here, the estimated HF hospitalization savings (~$500/patient-year) plus standard MACE and T2D offsets total roughly $870/patient-year against $8,400 in drug cost. The ROI remains negative in every identifiable subgroup.

2. The time horizon would need to extend well beyond typical employee tenure

Cardiovascular and metabolic benefits accrue slowly. Even in Scenario D, MACE offsets are $288 per starter at Year 1 and $5,760 at Year 20. Median tenure for covered employees is approximately 5 years (EBRI 2025, Current Population Survey data). By year 5, half of the original starters have left the plan. The payer who paid the drug cost is rarely the payer who would receive the medical offset.

There is also limited evidence that benefits persist after discontinuation. Real-world data shows that most patients who stop GLP-1 therapy regain 60-90% of lost weight within one year, with the BMJ meta-analysis projecting full return to baseline by 18 months. Cardiovascular and metabolic improvements track with weight and are expected to revert on a similar timeline. For more detail, see the weight regain reference page.

3. Benefits not modeled here would need to close a substantial gap

For Scenario D in the SELECT-eligible population to reach breakeven at 20 years at current pricing, unmodeled benefits would need to total roughly $6,272 per starter per year on an undiscounted 20-year average basis. For the FDA-label population, the figure is $7,829 per starter per year.

Productivity gains are excluded from this model and from standard cost-effectiveness analyses (Hwang, ICER, Hennessy) because no GLP-1-specific interventional productivity data has been published.

For each indication: clinical efficacy demonstrated in peer-reviewed RCTs. What is missing is payer-perspective dollar-offset data.

The sum of high-end sensitivity estimates across all categories approaches the $6,272 target. The sum of published, evidence-grade estimates does not.

4. Drug pricing would need to drop substantially

Even if conditions 1-3 were met, the drug still needs to be priced close to its medical offset. How far current pricing is from that point is the subject of the final section.

The breakeven price for medical savings alone

Setting aside unmodeled benefits, what would the drug need to cost for MACE and T2D savings alone to offset the drug spend?

In the FDA-label population under real-world conditions (Scenario A), the modeled medical savings total approximately $83 per patient-year on drug.

Drug cost: $8,400/year. Ratio: 101 to 1.

For the math to break even, the drug would need to cost $83 per year, or roughly $7 per month. That is not a rounding error. It is a category error in how broad GLP-1 coverage is being sold.

To be clear: this is not a claim that GLP-1 therapy is worth only $7/month to patients or to society. It is the narrow payer-budget breakeven for modeled MACE and T2D medical-claims offsets in the broad FDA-label population under real-world conditions. The societal value of the drug, including quality-of-life improvements, symptom relief, and mortality reduction, is substantially higher. But payers' pharmacy budgets do not capture that value.

At Scenario D (ideal dose and persistence indefinitely, where T2D savings accumulate year over year), the 20-year breakeven for the FDA-label population rises to $48 per month. The gap between $7 and $48 is almost entirely driven by T2D savings accumulation: when patients stay on drug for 20 years, each year's prevented T2D cases save $7,000/year for all remaining years, totaling $10,220 over 20 years. Under real-world persistence, patients stop by year 2-3 and that accumulation never happens.

| Population | Scenario | Medical savings per drug-year | Breakeven price | Current price | Multiple |

|---|---|---|---|---|---|

| SELECT | D (ideal) | $2,128/yr | $177/mo | $700/mo | 4× |

| SELECT | A (real-world) | $354/yr | $29/mo | $700/mo | 24× |

| FDA-label | D (ideal) | $571/yr | $48/mo | $700/mo | 15× |

| FDA-label | A (real-world) | $83/yr | $7/mo | $700/mo | 100× |

These breakeven prices reflect only MACE and T2D offsets. If unmodeled benefits were quantified and credited, breakeven prices would be higher. For Scenario D, the figure shown is the 20-year average including T2D accumulation.

A natural objection: "you picked a low MACE rate." The table below shows what happens if you make the inputs more favorable to the drug. Even doubling or tripling the base-case event rates does not bring the breakeven close to current pricing.

| Assumption set | MACE rate | T2D rate | Breakeven, real-world | Breakeven, Scenario D |

|---|---|---|---|---|

| Base case | 5/1,000 PY | 1.0%/yr | $7/mo | $48/mo |

| Higher-risk metabolicOlder, more comorbid | 10/1,000 PY | 2.0%/yr | $14/mo | $95/mo |

| Enriched primary preventionHigh prediabetes prevalence | 15/1,000 PY | 2.5%/yr | $19/mo | $121/mo |

| SELECT-like riskEstablished CVD | 24/1,000 PY | 3.6%/yr | $29/mo | $177/mo |

All breakeven prices for modeled MACE + T2D offsets only, 20-year horizon. Current modeled net drug price: $700/month.

What about improving persistence? Counterintuitively, higher persistence makes the ROI worse at current pricing. Under real-world conditions, each starter accumulates roughly 1.9 drug-years over 20 calendar years (most patients stop by year 2-3). If persistence improved to 5 drug-years per starter, net cost per starter in the FDA-label population would rise from ~$15,000 to ~$40,000, because you are buying 3× more drug while the savings per drug-year ($83) remain tiny relative to drug cost ($8,400). Discontinuation is currently capping the plan's financial exposure.

What about lower drug pricing? Novo Nordisk's Wegovy pill and Lilly's Foundayo are being offered through self-pay channels at roughly $149-$299/month depending on dose, timing, and program terms. Even at $299/month ($3,588/year), the ratio of drug cost to modeled medical offset is still 43:1 for the FDA-label population and 10:1 for SELECT-eligible. Only the SELECT Scenario D (ideal dose and persistence indefinitely) approaches breakeven at oral pricing, at a ratio of 1.7:1. Semaglutide composition-of-matter patents begin expiring ~2031-2032; generic pricing will depend on patent, manufacturing, and market dynamics.

What if unmodeled benefits are worth something? The breakeven prices above include only MACE and T2D. If productivity, OSA, knee OA, HFpEF, MASH, CKD, and recruitment/retention collectively add value, the breakeven rises. The question is how much.

| If other benefits are worth... | Breakeven rises to... | Gap to $700/mo |

|---|---|---|

| $0/yr (base case, MACE + T2D only) | $7/mo | 100× |

| $1,000/yr | $90/mo | 7.8× |

| $2,500/yr | $215/mo | 3.3× |

| $5,000/yr | $424/mo | 1.7× |

| $8,317/yr Required to justify current pricing | $700/mo | 1.0× |

FDA-label population, real-world persistence and dosing. "Other benefits" = any additional payer-captured medical or productivity savings per patient-year on drug. The highest published cross-sectional productivity estimate is $2,659/yr (Cawley et al.). OSA care avoidance at the high end could add ~$3,000/yr for affected patients. To reach current pricing, every benefit category would need to be at its maximum sensitivity estimate simultaneously.

Benefit, not investment

GLP-1 coverage is, at current pricing, structurally an employee benefit, not a cost-saving investment. This analysis does not argue that GLP-1s don't work. They do. It does not argue that no plan should cover them. Some will, for reasons that extend beyond pharmacy-budget arithmetic: employee experience, recruitment, the case for treating a chronic condition. But even at ideal conditions, the math does not produce a positive financial return at any plausible price point or time horizon. This is a pricing and structural constraint, not a failure of patient engagement or clinical management.

Plans that choose to cover GLP-1s should model them accordingly: as a benefit with a known cost, not as an investment with an expected return. If coverage is offered, tight eligibility gating is financially rational. And for the large majority of the coverage-eligible population who are not SELECT-eligible, population-scale weight management likely requires lower-cost interventions, tighter escalation criteria, or a different coverage architecture than indefinite broad GLP-1 use at current prices.

The drug works. The demand is real. The clinical value is substantial. But the broad ROI story depends on assumptions that current evidence does not support: high-risk event rates applied to low-risk populations, long-term benefits captured by short-tenure plans, and quality-of-life value treated as medical-claims savings. Until pricing, eligibility, and benefit design reflect that reality, broad GLP-1 coverage remains a highly valued employee benefit, not a self-funding medical-cost strategy.

This analysis builds on The Reality Gap. For supporting data and full citations, see the reference pages on cost, persistence, real-world outcomes, weight regain, and ROI.

Key to Health is an evidence-based behavioral weight management program. Published RCT data in 155 adults; 2-year real-world outcomes from 11,365 adults under peer review. Learn more about our employer program.